-

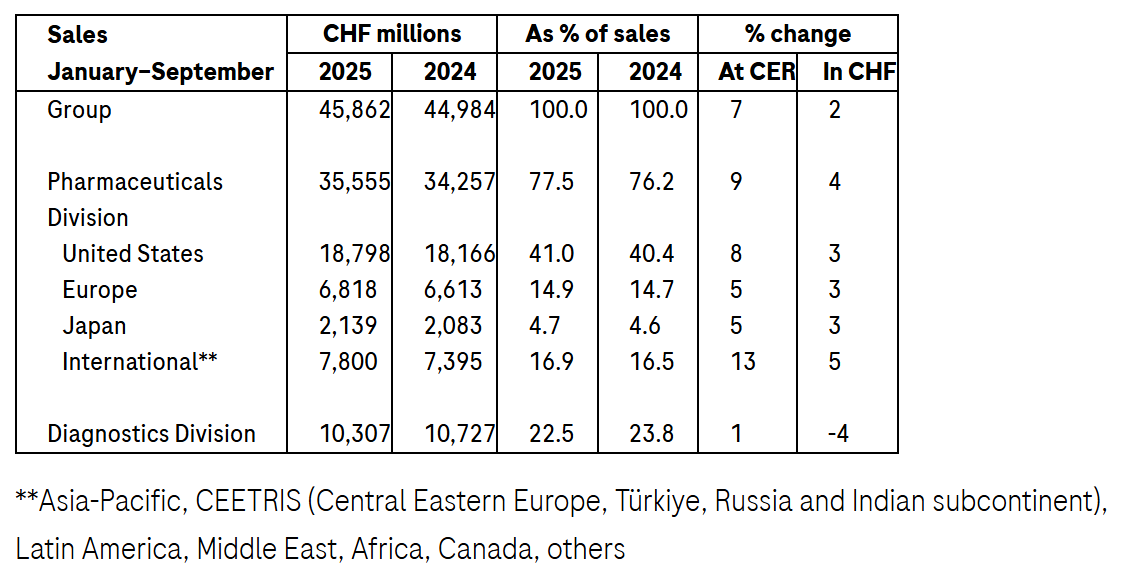

Group sales grew by 7%1 at constant exchange rates (CER; 2% in CHF) in the first nine months, driven by high demand for our innovative medicines and diagnostics.

-

Pharmaceuticals Division sales rose by 9% (4% in CHF) due to continued high growth in sales of medicines for the treatment of severe diseases; Phesgo (breast cancer), Xolair (food allergies), Hemlibra (haemophilia A), Vabysmo (serious eye diseases) and Ocrevus (multiple sclerosis) were the top growth drivers.

-

Diagnostics Division sales increased by 1% (-4% in CHF) as demand for pathology solutions and molecular diagnostics more than offset the impact of healthcare pricing reforms in China.

-

Highlights:

US approval for Tecentriq combination for a form of lung cancer and Gazyva/Gazyvaro for a severe kidney disease

EU CE mark for Contivue, a port delivery platform with Susvimo*, for a severe eye disease

Positive EU CHMP recommendation for the subcutaneous formulation of Lunsumio for a type of blood cancer and for Gazyva/Gazyvaro for a severe kidney disease

Positive data from phase III study on giredestrant in breast cancer, phase II open-label extension study on fenebrutinib in multiple sclerosis, phase I/II study on trontinemab in Alzheimer’s disease and long-term follow-up studies on Vabysmo and Susvimo in a severe age-related eye disease

Advancement of several key drug candidates into phase III trials: zilebesiran for uncontrolled hypertension, CT-388 for obesity, CT-868 for type 1 diabetes, cevostamab for a difficult-to-treat form of blood cancer and ZN-1041 for a type of breast cancer

Announcement of a merger agreement to acquire 89bio and its phase III FGF21 analogue for the treatment of moderate to severe metabolic dysfunction-associated steatohepatitis (MASH), a form of fatty liver disease that is one of the most prevalent comorbidities of obesity

EU CE mark and US approval for the Elecsys pTau181, the only FDA-cleared blood test for use in primary care to rule out Alzheimer’s disease-related amyloid pathology

EU CE mark for the first AI-based risk stratification tool to assess progressive decline in kidney function and for the sixth-generation Troponin T test, which shows a new level of accuracy critical in diagnosing heart attacks

-

Outlook for 2025 earnings raised.

Basel, 23 October 2025--Roche CEO Thomas Schinecker: “We continue to build on our positive momentum with strong sales growth of 7% at constant exchange rates.

Our momentum is further reflected in our pipeline with a number of positive clinical read-outs and a record ten potentially transformative medicines progressing into the final phase of development for diseases with significant unmet need. By the end of the decade, we expect phase III clinical results for up to 19 new medicines.

Our groundbreaking next-generation sequencing technology, set to launch next year, has achieved a new record for decoding a whole human genome in under four hours.

Based on our strong results, we are raising our earnings outlook for the full year.”

Outlook for 2025 earnings raised

Roche (SIX: RO, ROG; OTCQX: RHHBY) expects an increase in Group sales in the mid single digit range (CER). Core earnings per share are targeted to develop in the high single to low double digit range (CER). Roche expects to further increase its dividend in Swiss francs.

Group sales

In the first nine months of 2025, Roche achieved sales growth of 7% (2% in CHF) to CHF 45.9 billion due to strong demand for our pharmaceutical and diagnostic products.

The appreciation of the Swiss franc against most currencies, notably the US dollar, had an adverse impact on sales when reported in Swiss francs compared to constant exchange rates.

Sales in the Pharmaceuticals Division increased by 9% (4% in CHF) to CHF 35.6 billion, with medicines for severe diseases continuing their strong growth.

The top five growth drivers – Phesgo, Xolair, Hemlibra, Vabysmo and Ocrevus – achieved total sales of CHF 15.8 billion. This represents an increase of CHF 2.4 billion at CER compared to the first nine months of 2024.

This increase more than compensated for the total decrease of CHF 0.5 billion (CER) in sales of the ‘loss of exclusivity (LOE)’ products – the decline in sales of Avastin (various types of cancer), Herceptin (breast and gastric cancer), MabThera/Rituxan (blood cancer, rheumatoid arthritis), Lucentis (severe eye diseases) and Esbriet (lung disease) was partially offset by an increase in sales of Actemra/RoActemra (rheumatoid arthritis).

In the United States, sales rose by 8% due to growth in sales of Xolair, Phesgo, Ocrevus, Hemlibra, Polivy (blood cancer) and Vabysmo. This growth more than compensated for the decline in sales of medicines with expired patents.

Sales in Europe grew 5% as strong demand for Ocrevus and Vabysmo and the continuing uptake of Polivy, Phesgo and Hemlibra more than compensated for the lower sales of Perjeta (breast cancer) due to ongoing conversion of patients to Phesgo and the impact of biosimilar competition on Actemra/RoActemra sales.

In Japan, sales increased by 5%, mainly due to the strong uptake of Phesgo, Hemlibra, Vabysmo and PiaSky (paroxysmal nocturnal haemoglobinuria). Sales growth was partially offset by the decline in sales of Perjeta due to continued conversion of patients to Phesgo and of Avastin because of biosimilar erosion.

Sales in the International region grew by 13%, led by Phesgo, Hemlibra, Vabysmo, Xofluza (influenza) and Kadcyla (breast cancer). In China, sales rose by 9%, driven by the uptake of Phesgo due to inclusion in the government drug reimbursement list, strong sales of Xofluza and the continued roll-out of Polivy and Vabysmo.

The Diagnostics Division’s sales increased by 1% (-4% in CHF) to CHF 10.3 billion as growth in demand for pathology solutions and molecular diagnostics more than offset the impact of healthcare pricing reforms in China.

Sales in the Europe, Middle East and Africa (EMEA) region increased by 6%, driven by higher sales of clinical chemistry and immunodiagnostic products. In North America, sales increased by 7%, with growth across customer areas. Sales in Asia-Pacific decreased by 15% due to healthcare pricing reforms in China. Latin America sales grew by 14%.

About Roche

Founded in 1896 in Basel, Switzerland, as one of the first industrial manufacturers of branded medicines, Roche has grown into the world’s largest biotechnology company and the global leader in in-vitro diagnostics. The company pursues scientific excellence to discover and develop medicines and diagnostics for improving and saving the lives of people around the world. We are a pioneer in personalised healthcare and want to further transform how healthcare is delivered to have an even greater impact. To provide the best care for each person we partner with many stakeholders and combine our strengths in Diagnostics and Pharma with data insights from the clinical practice.

For over 125 years, sustainability has been an integral part of Roche’s business. As a science-driven company, our greatest contribution to society is developing innovative medicines and diagnostics that help people live healthier lives. Roche is committed to the Science Based Targets initiative and the Sustainable Markets Initiative to achieve net zero by 2045.

Genentech, in the United States, is a wholly owned member of the Roche Group. Roche is the majority shareholder in Chugai Pharmaceutical, Japan.

References

[1] Unless otherwise stated, all growth rates and comparisons to the previous year in this document are at constant exchange rates (CER: average rates 2024) and all total figures quoted are reported in CHF.

[2] Products launched before 2015.

[3] Core Lab: diagnostics solutions in the areas of immunoassays, clinical chemistry and CustomBiotech.

Molecular Lab: diagnostics solutions for pathogen detection and monitoring, donor screening, sexual health and genomics, genomic tumour profiling.

Near Patient Care: diagnostics solutions in emergency rooms, medical practices and directly with patients, including integrated personalised diabetes management.

Pathology Lab: diagnostics solutions for tissue biopsies and companion diagnostics.

In 2025, sales in the Pathology Lab customer area include sales previously reported in the Molecular Lab customer area to foster business transparency and harmonisation in the use of solutions in the area of cervical intraepithelial neoplasia technology (CINtec). The comparative information for 2024 has been restated accordingly.

In 2025, sales in the Core Lab customer area include sales previously reported in the Near Patient Care customer area to centralise digital healthcare solutions within Roche Information Solutions. The comparative information for 2024 has been restated accordingly.

* Susvimo is approved in the US by the Food and Drug Administration (FDA) for nAMD, diabetic macular edema (DME) and diabetic retinopathy (DR). It is currently under review with the European Medicines Agency (EMA) for the treatment of nAMD.