Sarepta announces completion of the confirmatory trial commitment for its ultra-rare disease PMO therapies AMONDYS 45 and VYONDYS 53:

-

While the ESSENCE study did not achieve statistical significance on its primary endpoint, results indicate positive and encouraging trends favoring therapy at 96 weeks

-

Sarepta reports that the study was impacted by the COVID-19 pandemic and, when COVID-impacted data is excluded, meaningful treatment effect is seen on the primary endpoint

-

ESSENCE supported favorable safety profile of AMONDYS 45 and VYONDYS 53

-

The Company intends to schedule a meeting with FDA to discuss path to a traditional approval based on the positive risk-benefits of the therapies from the results of the ESSENCE study and significant positive multi-year real-world evidence

Net product revenues for the third quarter 2025 totaled $370.0 million, consisting of $238.5M of PMO and $131.5M of ELEVIDYS

Refinancing of a majority portion of 2027 Notes and cost restructuring initiatives strengthened overall financial position

ELEVIDYS labeling discussions progressing and expected to be concluded soon

Presentations at 2025 World Muscle Society congress added to the body of evidence regarding ELEVIDYS safety and efficacy

CAMBRIDGE, Mass.--(BUSINESS WIRE)--Nov. 3, 2025-- Sarepta Therapeutics, Inc. (NASDAQ:SRPT), the leader in precision genetic medicine for rare diseases, today reported financial results for the third quarter of 2025 and the completion of ESSENCE, its global, Phase 3 randomized, double-blind, placebo-controlled study evaluating the efficacy and safety of AMONDYS 45 (casimersen) and VYONDYS 53 (golodirsen) compared to placebo in 225 patients, ages 6-13 years old, with Duchenne muscular dystrophy (Duchenne) amenable to exon 45 or 53 skipping.

Topline Results from ESSENCE

Topline results found that numerical trends favored treatment versus placebo; however, the observed difference of 0.05 steps/second in least square means (LSM), did not reach statistical significance (P=0.309) on the primary endpoint, the 4-step ascend velocity at 96 weeks.

The ESSENCE study was conducted over a nine-year period that included the COVID-19 pandemic, which impacted study participants and outcomes. An analysis that excludes data from participants whose double-blind period overlapped with the COVID-19 pandemic (n=57), shows a 30% reduction (LSM 0.11 steps/second, P=0.09) in disease progression over 2 years on the 4-step ascend velocity in non-COVID impacted treated participants versus placebo (n=168). This is a clinically meaningful change.

There were no new safety signals in the ESSENCE study, reinforcing the favorable and stable safety profile observed with exon-skipping therapies over years. Adverse events were mostly mild (88%) or moderate (10.3%) and comparable between treatment and placebo groups. The most common treatment-emergent adverse events (≥10%) were vomiting, nasopharyngitis, pyrexia, headache, cough, fall, and upper respiratory infections.

For more than a decade, Sarepta’s PMO (phosphorodiamidate morpholino oligomer) therapies have been used to treat over 1,800 amenable patients worldwide, from infants as young as 7 months to adults well into their 30s. The results from ESSENCE add to the available evidence for VYONDYS 53 and AMONDYS 45, including real-world studies demonstrating, for instance, that treatment with VYONDYS 53 is associated with a 7.5 year delay in the need for nighttime ventilation1 and treatment with AMONDYS 45 is associated with a statistically significant slowing of lung function decline and a potentially meaningful benefit in the predicted time to use of a cough assist device2. Across our PMO portfolio, real-world evidence indicates a multi-year benefit on mortality3,4, delays in time to loss of ambulation of 3 and 4 years5,6, a substantial reduction in risk of reaching a left ventricular ejection fraction (LVEF) of less than 55%7, and a significant reduction in emergency room and other hospital visits8.

Based on the encouraging trends seen in ESSENCE, the substantial real-world evidence, and the positive safety profile of AMONDYS 45 and VYONDYS 53, Sarepta intends to schedule a meeting with the U.S. Food and Drug Administration (FDA) to discuss the possibility of converting from accelerated to traditional approval.

Sarepta continues to analyze the results from ESSENCE and, together with real-world evidence, full results will be submitted to the FDA as part of the planned sNDA filings for these two exon-skipping therapies. The completion of the ESSENCE study is expected to fulfill the primary postmarketing requirement. Additionally, results from ESSENCE will be shared at future medical meetings, and publication will be pursued in a medical journal.

“While the ESSENCE study did not meet statistical significance on its primary endpoint, we believe the results demonstrated a clear treatment effect, showing clinically meaningful functional outcomes for people with Duchenne who have mutations amenable to skipping exons 45 or 53. These topline findings reinforce the potential impact of these therapies to slow muscle weakness and other symptoms. The results of the study are consistent with the growing body of real-world evidence accumulated over several years. These data, which we have shared with the FDA, strengthen our confidence in the benefit of added dystrophin over time,” said Louise Rodino-Klapac, Ph.D., president of research & development and technical operations, Sarepta.

Dr. Rodino-Klapac continued, “This trial enrolled an ultra-rare subset of eligible Duchenne patients. The complexity of Duchenne, combined with the heterogeneity of the population and the impact of the COVID pandemic on participation, made this an extraordinary undertaking. We are deeply grateful to the families and investigators whose dedication made this possible, and we remain committed to advancing care for the Duchenne community by delivering options that can change the course of Duchenne.”

“In the trial and my clinical practice, I’ve followed boys and young men treated with casimersen and golodirsen since their initial approvals and, in my opinion, these therapies can help preserve critical functions like walking, stair climbing and feeding themselves. Over time, these gains can translate into a delayed loss of ambulation and even slower respiratory decline, potentially offering these individuals a meaningful path to maintaining quality of life," said Craig McDonald, M.D., professor and chair of the UC Davis Health Department of Physical Medicine and Rehabilitation, and an investigator in the ESSENCE study.

Business Highlights for the Quarter Ended Sept. 30, 2025

“We are pleased to have met our primary post-marketing obligation with the completion of ESSENCE, a particularly challenging trial to execute in the context of these ultra-rare diseases that heterogeneously degenerate over the course of decades. We look forward to discussing the ESSENCE results and the real-world evidence for AMONDYS 45 and VYONDYS 53 with the FDA,” stated Doug Ingram, chief executive officer, Sarepta.

Mr. Ingram continued, “We are also pleased to report solid performance in the quarter from our gene therapy, ELEVIDYS, and our three PMOs, EXONDYS 51, VYONDYS 53 and AMONDYS 45. Our net product revenue stood at $370.0 million for the quarter. Additionally, having taken steps to bolster our financial position, including the refinancing of our convertible debt and a significant financial restructuring, I am pleased to report positive cash flow in the quarter. Looking forward, we have a strong financial position from which to continue to serve our community as we advance a very exciting siRNA portfolio.”

-

ELEVIDYS (delandistrogene moxeparvovec-rokl) Regulatory Discussions: Discussions between FDA and Sarepta in the safety labeling process are expected to be finalized in the near-term with an outcome that includes a box warning and the removal of non-ambulatory indication from the Indication and Usages section of the Prescribing Information. Discussions with FDA are also ongoing regarding Sarepta’s proposed study to evaluate an additional immunosuppression regimen toward re-including non-ambulatory in the label.

-

Pipeline progress for multiple siRNA programs: Readouts of FSHD and DM1 phase 1/2 studies from both SAD and MAD cohorts expected in early 2026.

Facioscapulohumeral muscular dystrophy (FSHD): Phase 1/2 study of SRP-1001 enrollment of the SAD is complete and cohort 6 of MAD is ongoing.

Myotonic dystrophy type 1 (DM1): Phase 1/2 study of SRP-1003 enrollment of the SAD is complete and cohort 4 of the MAD is ongoing.

Huntington’s Disease (HD): On track to initiate clinical trial for SRP-1005 by end of 2025 utilizing subcutaneous route of administration.

Research target selection: Three new research targets have been selected in addition to second-generation DM1 candidate selected at close of Arrowhead deal.

-

2025 World Muscle Society (WMS): At the WMS meeting, Sarepta presented new data on ELEVIDYS, as well as updates from our PMO and LGMD 2E programs. Additionally, multiple independent studies were presented, including preliminary analysis of safety, tolerability and efficacy of a prophylactic sirolimus protocol for patients receiving delandistrogene moxeparvovec-rokl gene therapy. All posters and presentations from the WMS meeting are available on the Company’s website here.

-

Financial Foundation: The Company has taken steps this quarter to further strengthen its financial foundation by extending the maturity of a meaningful portion of its convertible notes to 2030, enhancing liquidity with the disposition of its Arrowhead equity investment, and achieving expense savings above stated cost restructuring targets.

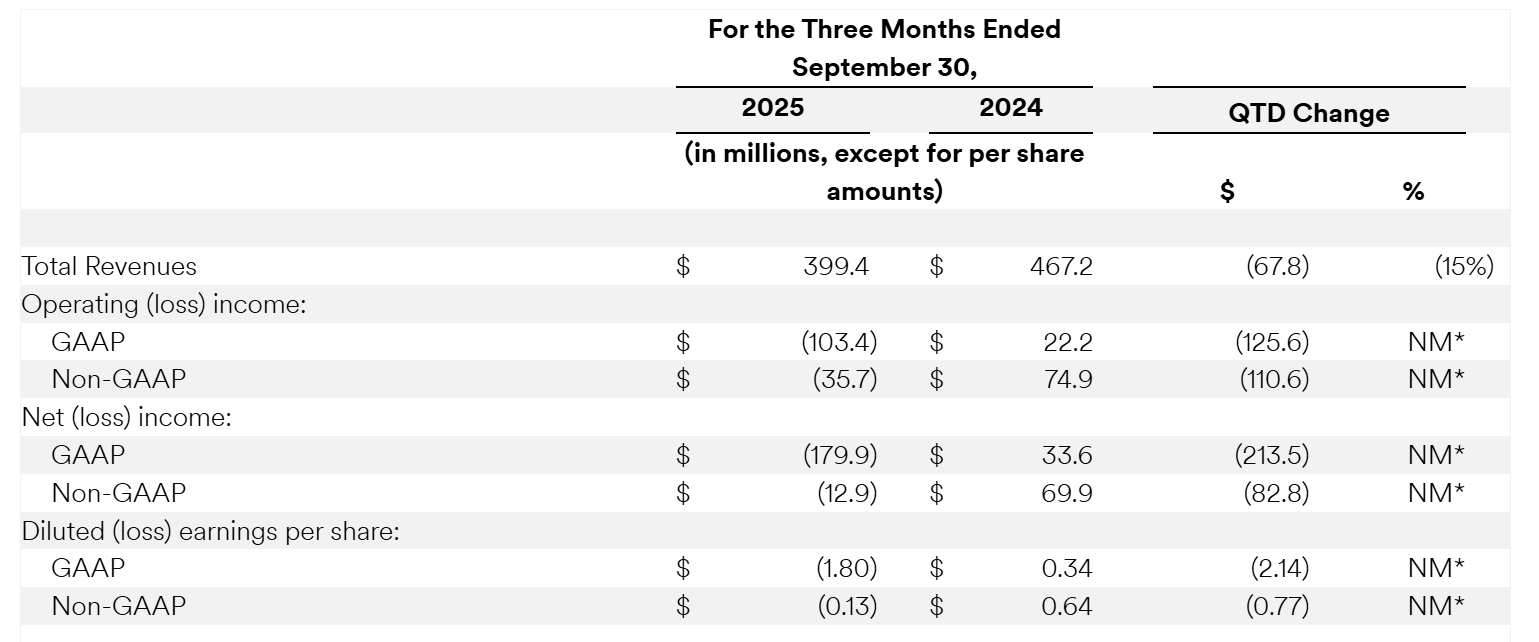

Q3 2025 Financial Highlights1

Revenues

Total revenues were $399.4 million for the three months ended September 30, 2025, as compared to $467.2 million for the same period of 2024, a decrease of $67.8 million. The decrease primarily reflects $49.5 million less in net product revenue of ELEVIDYS as a result of lower volume following our decision to suspend shipments of ELEVIDYS to non-ambulatory patients in the U.S. in June 2025. In addition, other revenues decreased $8.1 million primarily due to contract manufacturing revenues decreasing $9.2 million driven by a lower volume of shipments of ELEVIDYS to Roche.

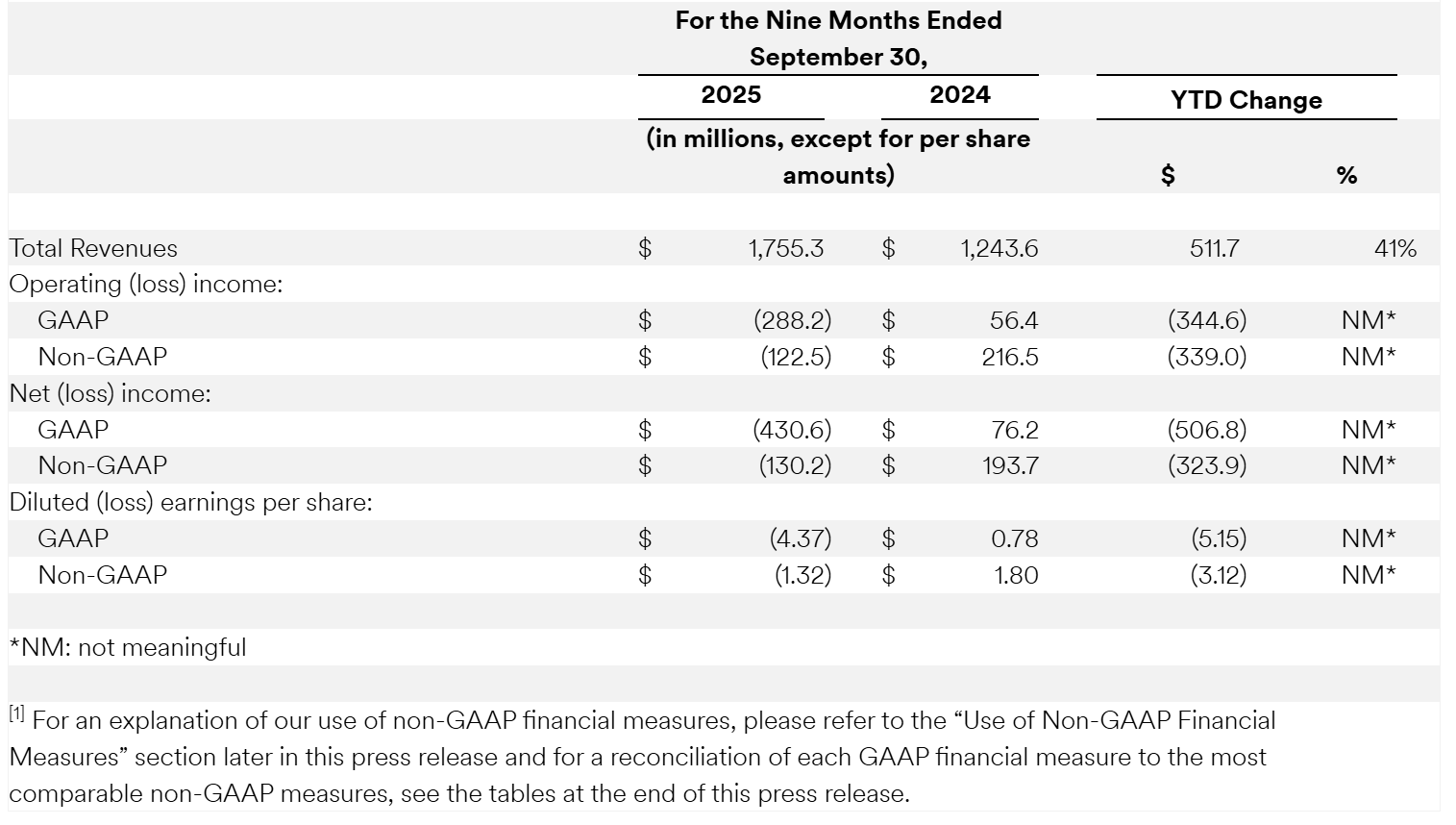

Total revenues were $1,755.3 million for the nine months ended September 30, 2025, as compared to $1,243.6 million for the same period of 2024, an increase of $511.7 million. The increase primarily reflects $351.7 million more in net product revenue of ELEVIDYS as a result of its expanded label approval in June 2024. In addition, collaboration and other revenues increased approximately $166.9 million primarily related to the $63.5 million of collaboration revenue recognized as a result of regulatory approval in Japan and the $112.0 million of collaboration revenue recognized related to Roche's expiration of an option for a program during the nine months ended September 30, 2025, as compared to $48.0 million of collaboration revenue recognized in the same period of 2024 related to Roche’s declined option to acquire certain ex-US rights to an external, early-stage Duchenne development program. Furthermore, contract manufacturing revenues and royalty revenues increased $29.4 million and $9.9 million, respectively, associated with an increase in commercial ELEVIDYS supply delivered to Roche as well as royalty revenue from sales of ELEVIDYS by Roche, respectively.

Cost of sales (excluding amortization of in-licensed rights)

Cost of sales (excluding amortization of in-license rights) were $150.8 million for the three months ended September 30, 2025, as compared to $91.7 million for the same period of 2024, an increase of approximately $59.1 million. The increase primarily reflects the depletion of previously expensed ELEVIDYS inventory, the impairment of prepaid manufacturing deposits and an increase in the write-offs of certain batches of our products not meeting our quality specifications for the three months ended September 30, 2025, as compared to the same period of 2024. Cost of sales (excluding amortization of in-license rights) were $440.9 million for the nine months ended September 30, 2025, as compared to $186.8 million for the same period of 2024, an increase of $254.1 million. The increase primarily reflects an increased demand for ELEVIDYS following the expanded label approval in June 2024, the depletion of previously expensed ELEVIDYS inventory, an increase in the write-offs of certain batches of our products not meeting our quality specifications, an increase in products sold to Roche under the Roche collaboration agreement and the impairment of prepaid manufacturing deposits for the nine months ended September 30, 2025, as compared to the same period of 2024.

Operating expenses and others

Research and development expenses were $218.9 million for the three months ended September 30, 2025, as compared to $224.5 million for the same period of 2024, a decrease of $5.6 million. The decrease is primarily due to a $102.7 million decrease in manufacturing expenses predominantly as a result of costs associated with the termination of our development, commercial manufacturing and supply agreement with Brammer Bio MA, LLC, an affiliate of Thermo Fisher Scientific, Inc. (Thermo Agreement) during the three months ended September 30, 2024, with no similar activity for the three months ended September 30, 2025, as well as a decrease in compensation, other personnel, and stock-based compensation expenses as a result of our restructuring plan announced during the three months ended September 30, 2025. This decrease was partially offset by a $100.0 million increase in up-front and milestone expenses due to our milestone payment to Arrowhead, triggered by Arrowhead's achievement of the first of two predetermined enrollment targets and subsequent authorization to dose escalate in a Phase 1/2 study for the DM1 program, with no similar activity for the three months ended September 30, 2024. For the three months ended September 30, 2025, non-GAAP research and development expenses were $206.5 million, as compared to $199.8 million for the same period of 2024, an increase of $6.7 million.

Research and development expenses were $1,196.7 million for the nine months ended September 30, 2025, as compared to $604.6 million for the same period of 2024, an increase of approximately $592.1 million. The increase primarily reflects a $583.6 million increase in up-front and milestone expense associated with the licensing and collaboration agreement and stock purchase agreement with Arrowhead, as well as the $100.0 million milestone payment made to Arrowhead for the nine months ended September 30, 2025, partially offset by a decrease of $74.9 million in manufacturing expenses primarily due to the termination of the Thermo Agreement during the nine months ended September 30, 2024, as well as a decrease in compensation, other personnel, and stock-based compensation expenses as a result of our restructuring plan in July 2025. For the nine months ended September 30, 2025, non-GAAP research and development expenses were $1,137.4 million, as compared to $531.8 million for the same period of 2024, an increase of $605.6 million.

Selling, general and administrative expenses were $91.9 million for the three months ended September 30, 2025, as compared to $128.2 million for the same period of 2024, a decrease of $36.3 million. The decrease is primarily driven by lower compensation and other personnel expenses due to reduced headcount, as well as a decrease in stock-based compensation due to the reversal of previously recognized expense related to unvested awards, all as a result of our restructuring plan announced in July 2025. For the three months ended September 30, 2025, non-GAAP selling, general and administrative expenses were $77.1 million, as compared to $100.2 million for the same period of 2024, a decrease of $23.1 million.

Selling, general and administrative expenses were $363.4 million for the nine months ended September 30, 2025, as compared to $394.0 million for the same period of 2024, a decrease of $30.6 million. The decrease is primarily driven by reduced headcount as a result of our restructuring plan for the nine months ended September 30, 2025 and a net decrease in stock-based compensation primarily due to the achievement of performance conditions related to certain PSUs during the nine months ended September 30, 2024, and the reversal of previously recognized expense related to unvested awards as a result of our restructuring plan announced in July 2025, partially offset by the fulfillment of remaining service conditions associated with certain PSUs in March 2025. For the nine months ended September 30, 2025, non-GAAP selling, general and administrative expenses were $297.6 million, as compared to $306.7 million for the same period of 2024, a decrease of $9.1 million.

Restructuring charges were $40.5 million for the three and nine months ended September 30, 2025, with no similar activity for the same periods of 2024. These charges were primarily related to employee termination benefits, including severance, along with accelerated depreciation for assets impacted by our restructuring plan, announced in July 2025, that was designed to reduce operating expenses and align our cost structure with strategic priorities, aiming to enhance financial flexibility and meet our 2027 financial obligations.

Loss on debt extinguishment was $138.6 million for the three and nine months ended September 30, 2025, with no similar activity for the same periods of 2024. The loss on debt extinguishment is a result of our partial refinancing of the 2027 Notes through a privately negotiated exchange transaction where we exchanged $700.0 million in aggregate principal amount of 2027 Notes for (1) $602.0 million in aggregate principal amount of new convertible senior notes due on September 1, 2030 (the “2030 Notes”), net of issuance costs of $13.4 million, (2) cash payments of $127.3 million, including $4.0 million of accrued interests, and (3) the issuance of 5.9 million shares of our common stock with fair market value of approximately $107.3 million, net of issuance costs of $2.4 million.

Other income, net for the three months ended September 30, 2025 and 2024, was $48.0 million and $11.8 million, respectively. The change primarily reflects the fair value adjustments of our investments, including Arrowhead, during the three months ended September 30, 2025. Other income, net for the nine months ended September 30, 2025 and 2024, was $2.9 million and $32.6 million, respectively. The change primarily reflects the decrease in interest income due to changes in the investment mix of our investment portfolio and the fair value adjustments of our investments in Arrowhead during the nine months ended September 30, 2025.

Income tax (benefit) expense for the three months ended September 30, 2025 and 2024, was $(14.1) million and $0.4 million, respectively. Income tax expense for the nine months ended September 30, 2025 and 2024, was $6.6 million and $12.8 million, respectively. Income tax benefit for the three months ended September 30, 2025, relates to the tax benefit recorded on the quarter to date loss which offsets tax expense recorded on profits in prior interim periods. Income tax expense for the nine months ended September 30, 2025, as well as for the three and nine months ended September 30, 2024, primarily relates to state, federal and foreign income taxes for which available tax losses or credits were not available to offset.

Use of Non-GAAP Measures

In addition to the GAAP financial measures set forth in this press release, we have included the following non-GAAP measurements:

-

Non-GAAP net (loss) income is defined by us as GAAP net (loss) income excluding interest income/expense, net, depreciation and amortization expense, stock-based compensation expense, restructuring charges, other items and the estimated income tax impact of each pre-tax non-GAAP adjustment.

-

Non-GAAP net loss per share is defined by us as non-GAAP net loss, as defined above, divided by the weighted-average number of shares of common stock outstanding as the inclusion of dilutive common stock equivalents outstanding is anti-dilutive. Non-GAAP earnings per share is defined by us as non-GAAP net income, as defined previously, divided by the weighted-average number of shares of common stock and dilutive common stock equivalents outstanding, adjusted for the inclusion of additional shares under the “if-converted” method, if applicable and not anti-dilutive.

-

Non-GAAP operating (loss) income is defined by us as GAAP operating (loss) income excluding depreciation and amortization expense, stock-based compensation expense, and restructuring charges.

-

Non-GAAP research and development expenses are defined by us as GAAP research and development expenses excluding depreciation and amortization expense, and stock-based compensation expense.

-

Non-GAAP selling, general and administrative expenses are defined by us as GAAP selling, general and administrative expenses excluding depreciation expense, stock-based compensation expense and other items.

The following components are used to adjust our GAAP financial measures into the previously defined non-GAAP measurements:

-

Interest, depreciation and amortization - Interest income (expense), net amounts can vary substantially from period to period due to changes in cash and debt balances and interest rates driven by market conditions outside of our operations. Depreciation expense can vary substantially from period to period as the purchases of property and equipment may vary significantly from period to period and without any direct correlation to our operating performance. Amortization expense primarily associated with patent costs are amortized over a period of several years after acquisition or patent application or renewal.

-

Stock-based compensation expenses - Stock-based compensation expenses represent non-cash charges related to equity awards we have granted. Although these are recurring charges to operations, we believe the measurement of these amounts can vary substantially from period to period and depend significantly on factors that are not a direct consequence of operating performance that is within our control. Therefore, we believe that excluding these charges facilitates comparisons of our operational performance in different periods.

-

Restructuring charges do not have a direct correlation to future business operations, nor do the resulting charges recorded reflect the performance of our ongoing operations for the period in which such charges are recorded. In addition, restructuring charges are not considered to be normal operating expenses due to the variability of amounts and lack of predictability as to occurrence and/or timing.

-

Other items - We evaluate other items of expense and income on an individual basis. We take into consideration quantitative and qualitative characteristics of each item, including (a) nature, (b) whether the items relate to our ongoing business operations, and (c) whether we expect the items to continue or occur on a regular basis. These other items include the gain/loss on strategic investments, changes in the fair value of derivatives, restructuring charges, and loss on debt extinguishment and may include other items that fit the above characteristics in the future. We exclude from our non-GAAP results:

-

The (gain) loss on strategic investments as results of such gains and losses are not representative of our normal business operations, which accordingly, would make it difficult to compare our results to peer companies that also provide non-GAAP disclosures. We are making this change beginning in 2025 because, as our strategic investments have increased, we recognized that the resulting variability can impede comparability between periods of our financial performance for our ongoing business operations.

-

The change in fair value of derivatives related to regulatory-related contingent payments meeting the definition of a derivative to

-

Myonexus Therapeutics, Inc.

-

selling shareholders as well as to an academic institution under a separate license agreement as these are non-cash items and are not considered to be normal operating expenses due to the variability of amounts and lack of predictability as to occurrence and/or timing.

-

The loss on debt extinguishment is considered to be an infrequent event as it is associated with a distinct financing decision and is not indicative of the performance of our core operations, which accordingly would make it difficult to compare the our results to peer companies that also provide non-GAAP disclosures.

We use these non-GAAP measures as key performance measures for the purpose of evaluating operational performance and cash requirements internally. We also believe these non-GAAP measures increase comparability of period-to-period results and are useful to investors as they provide a similar basis for evaluating our performance as is applied by management. These non-GAAP measures are not intended to be considered in isolation or to replace the presentation of our financial results in accordance with GAAP. Use of the terms non-GAAP research and development expenses, non-GAAP selling, general and administrative expenses, non-GAAP operating (loss) income, non-GAAP net (loss) income, and non-GAAP diluted (loss) earnings per share may differ from similar measures reported by other companies, which may limit comparability, and are not based on any comprehensive set of accounting rules or principles. All relevant non-GAAP measures are reconciled from their respective GAAP measures in the attached table “Reconciliation of GAAP Financial Measures to Non-GAAP Financial Measures.”

About EXONDYS 51

EXONDYS 51 uses Sarepta’s proprietary phosphorodiamidate morpholino oligomer (PMO) chemistry and exon-skipping technology to bind to exon 51 of dystrophin pre-mRNA, resulting in exclusion, or “skipping”, of this exon during mRNA processing in patients with genetic mutations that are amenable to exon 51 skipping. Exon skipping is intended to allow for production of an internally truncated dystrophin protein.

EXONDYS 51 is indicated for the treatment of Duchenne muscular dystrophy (DMD) in patients who have a confirmed mutation of the DMD gene that is amenable to exon 51 skipping. This indication is approved under accelerated approval based on an increase in dystrophin in skeletal muscle observed in some patients treated with EXONDYS 51. Continued approval for this indication may be contingent upon verification of a clinical benefit in confirmatory trials.

EXONDYS 51 has met the full statutory standards for safety and effectiveness and as such is not considered investigational or experimental.

About VYONDYS 53

VYONDYS 53 (golodirsen) uses Sarepta’s proprietary phosphorodiamidate morpholino oligomer (PMO) chemistry and exon-skipping technology to bind to exon 53 of dystrophin pre-mRNA, resulting in exclusion, or “skipping,” of this exon during mRNA processing in patients with genetic mutations that are amenable to exon 53 skipping. Exon skipping is intended to allow for production of an internally truncated dystrophin protein.

VYONDYS 53 is indicated for the treatment of Duchenne muscular dystrophy (DMD) in patients who have a confirmed mutation of the DMD gene that is amenable to exon 53 skipping. This indication is approved under accelerated approval based on an increase in dystrophin production in skeletal muscle observed in patients treated with VYONDYS 53. Continued approval for this indication may be contingent upon verification of a clinical benefit in confirmatory trials.

VYONDYS 53 has met the full statutory standards for safety and effectiveness and as such is not considered investigational or experimental.

About AMONDYS 45

AMONDYS 45 (casimersen) uses Sarepta’s proprietary phosphorodiamidate morpholino oligomer (PMO) chemistry and exon-skipping technology to bind to exon 45 of dystrophin pre-mRNA, resulting in exclusion, or “skipping,” of this exon during mRNA processing in patients with genetic mutations that are amenable to exon 45 skipping. Exon skipping is intended to allow for production of an internally truncated dystrophin protein.

AMONDYS 45 is indicated for the treatment of Duchenne muscular dystrophy (DMD) in patients who have a confirmed mutation of the DMD gene that is amenable to exon 45 skipping. This indication is approved under accelerated approval based on an increase in dystrophin production in skeletal muscle observed in patients treated with AMONDYS 45. Continued approval for this indication may be contingent upon verification of a clinical benefit in confirmatory trials.

AMONDYS 45 has met the full statutory standards for safety and effectiveness and as such is not considered investigational or experimental.

About ELEVIDYS (delandistrogene moxeparvovec-rokl)

ELEVIDYS (delandistrogene moxeparvovec-rokl) is a single-dose, adeno-associated virus (AAV)-based gene transfer therapy for intravenous infusion designed to address the underlying genetic cause of Duchenne muscular dystrophy – mutations or changes in the DMD gene that result in the lack of dystrophin protein – through the delivery of a transgene that codes for the targeted production of ELEVIDYS micro-dystrophin in skeletal muscle.

ELEVIDYS is indicated for the treatment of Duchenne muscular dystrophy (DMD) in individuals at least 4 years of age.

For patients who are ambulatory and have a confirmed mutation in the DMD gene

For patients who are non-ambulatory and have a confirmed mutation in the DMD gene.

The DMD indication in non-ambulatory patients is approved under accelerated approval based on expression of ELEVIDYS micro-dystrophin (noted hereafter as “micro-dystrophin”) in skeletal muscle. Continued approval for this indication may be contingent upon verification and description of clinical benefit in a confirmatory trial(s).

About Sarepta Therapeutics

Sarepta is on an urgent mission: engineer precision genetic medicine for rare diseases that devastate lives and cut futures short. We hold a leadership position in Duchenne muscular dystrophy (Duchenne) and are building a robust portfolio of programs across muscle, central nervous system, and cardiac diseases.

1 Iff J, et al. Delayed Pulmonary Progression in Golodirsen-Treated Patients With Duchenne Muscular Dystrophy vs Mutation-Matched External Controls. Presented at MDA 2024.

2 Kuntz N, et al. Pulmonary Function in Advanced-Stage Patients With Duchenne Muscular Dystrophy Treated With Casimersen. Presented at WMS 2025.

3 Iff J, , et al. Survival among patients receiving eteplirsen for up to 8 years for the treatment of Duchenne muscular dystrophy and contextualization with natural history controls. Muscle & Nerve. 2024; 70(1): 60-70. doi:10.1002/mus.28075.

4 Data on file.

5 Mathews K, et al. Comparative Analysis of Loss of Ambulation in Eteplirsen-Treated Patients With DMD in the EVOLVE Study and Propensity Score–Weighted External Controls. Presented at MDA 2025.

6 Muntoni F, et al. Comparing Ambulatory Outcomes of Golodirsen-Treated Patients vs Mutation-Matched External Controls. Presented at CNS 2025.

7 Iff J, et al. Association Between Exon-Skipping Therapy With Eteplirsen and Cardiac Outcomes in Duchenne Muscular Dystrophy. Presented at MDA 2025.

8 Iff J, et al. Journal Comp Eff Res. 2023 Sep;12(9):e230086. doi: 10.57264/cer-2023-0086.