Paris, January 29, 2026

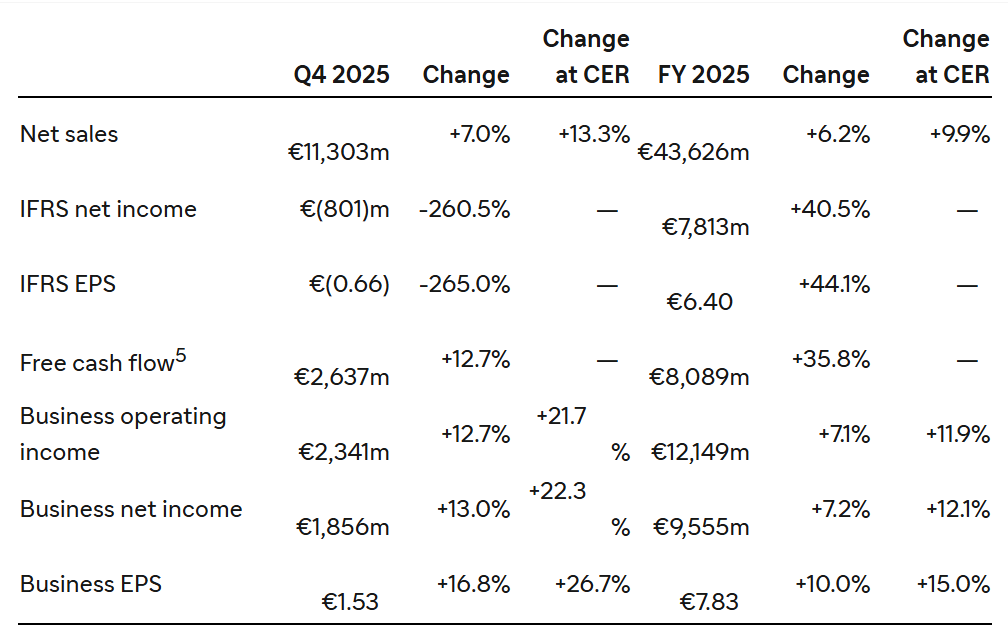

Q4 sales growth of 13.3% at CER1 and business earnings per share (EPS)2 of €1.53

-

Pharma launches increased sales by 49.4%, reaching €1.1 billion, primarily driven by Ayvakit and ALTUVIIIO

-

Dupixent sales increased by 32.2% to €4.2 billion, a strong end to the year

-

Vaccines sales decreased by 2.5% to €2.0 billion, with influenza performing better than anticipated

-

Research and Development expenses reached €2.3 billion, up by 6.6%

-

Selling, general and administrative expenses reached €2.7 billion, up by 9.6%, supporting launches

-

Business EPS was €1.53, up by 26.7% at CER; 16.8% at actual exchange rates, delivering profitable growth; IFRS EPS -€0.66

Pipeline progress

-

Ten regulatory approvals across immunology, rare diseases, and other

-

Positive phase 3 readouts: amlitelimab program in AD (COAST 2, SHORE) and Dupixent in AFRS

Tolebrutinib in PPMS did not meet the primary endpoint -

Four regulatory submission acceptances, five phase 3 study starts, three regulatory designations (orphan, priority reviews)

Capital allocation

-

Announcement of the Dynavax acquisition3 and completion of the Vicebio acquisition

-

Completion of the €5 billion share buyback program

-

Proposed dividend of €4.12; up by 5.1%

Other major developments

-

Sanofi reached agreement with the US government to lower medicine costs while strengthening innovation

-

Sanofi leads an industry working group on biopharma life cycle assessment

Guidance

-

In 2026, sales are expected to grow by a high single-digit percentage at CER. Business EPS at CER is expected to grow slightly faster than sales (before share buyback), delivering profitable growth.4 Sanofi intends to execute a share buyback program in 2026 of €1 billion.

Paul Hudson, Chief Executive Officer: “In the fourth quarter, sales growth accelerated to 13.3%, delivering another strong performance. Growth was supported by new medicines and Dupixent, reaching a new quarterly high. Business EPS was up by 26.7% with the benefit of cost discipline and growth leverage. We obtained ten regulatory approvals across immunology, rare diseases, and other, and had several positive phase 3 readouts.

In 2025, we achieved a strong year of profitable growth. Sales increased by 9.9% at constant exchange rates, while business EPS improved significantly faster by 15.0%. We launched three new medicines and vaccines: Qfitlia, Wayrilz, and Nuvaxovid, providing innovative options to patients with rare diseases and COVID-19 prevention. All this was made possible by the dedicated effort of all Sanofi colleagues worldwide.

In 2026, we expect sales to grow by a high single-digit percentage and business EPS to grow slightly faster than sales. We anticipate profitable growth to continue over at least five years.”

1 Changes in net sales are at constant exchange rates (CER) unless stated otherwise (definition in Appendix 9).

2 To facilitate an understanding of operational performance, Sanofi comments on the business net income, a non-IFRS financial measure (definition in

Appendix 9). The income statement is in Appendix 3 and a reconciliation of IFRS net income to business net income is in Appendix 4.

3 The acquisition of Dynavax is currently pending; it is expected to close in Q1 2026 subject to the satisfaction of customary closing conditions.

4 Applying January 2026 average currency exchange rates, the currency impacts are estimated at c.-2% on sales and at c.-3% on business EPS.

5 Free cash flow is a non-IFRS financial measure (definition in Appendix 9).