Despite a slight rebound in Q4, Chinese biopharma financing in 2024 continued its downward trend. According to data gathered by PharmaDJ, Chinese biopharmaceutical companies raised a disclosed total of $3.3 billion across 155 deals—a 31% drop from $4.8 billion in 2023 and a 59% decrease from $8.1 billion in 2022. 20 deals remained undisclosed.

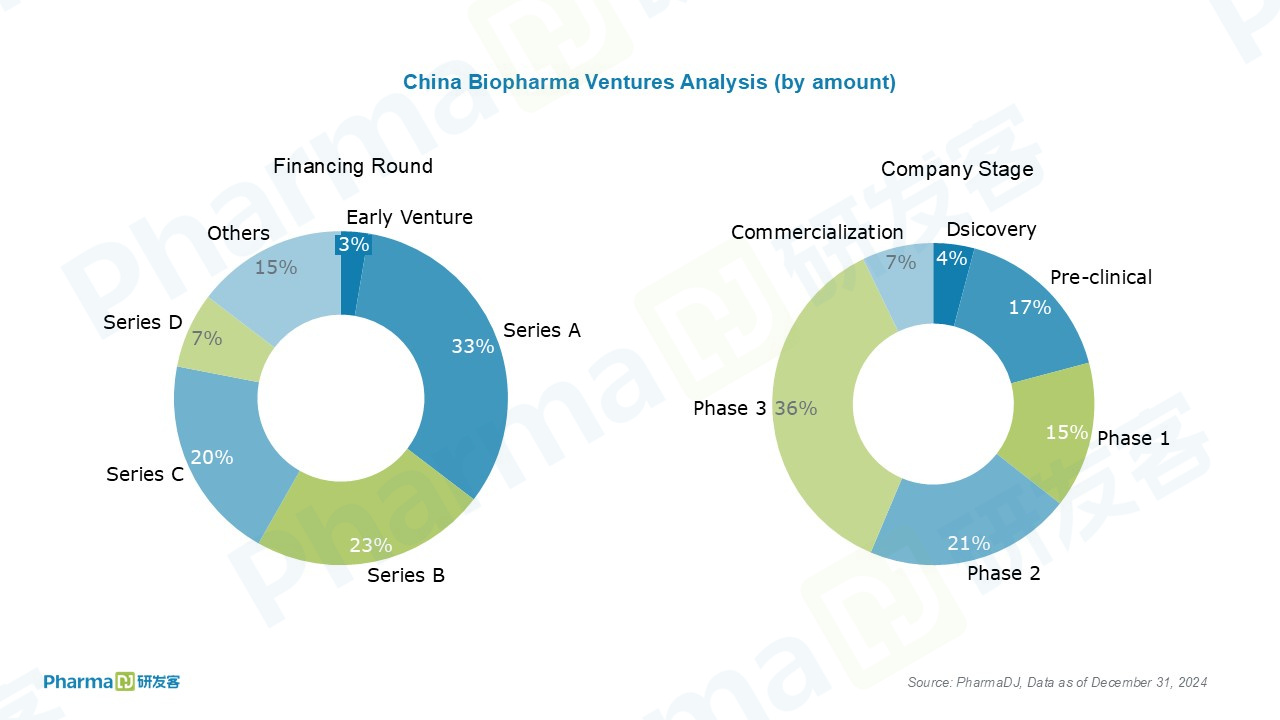

Of the total financing, $1.2 billion (36%) came from U.S. funds, with Series A and Phase 3-stage companies capturing the majority of the funding.

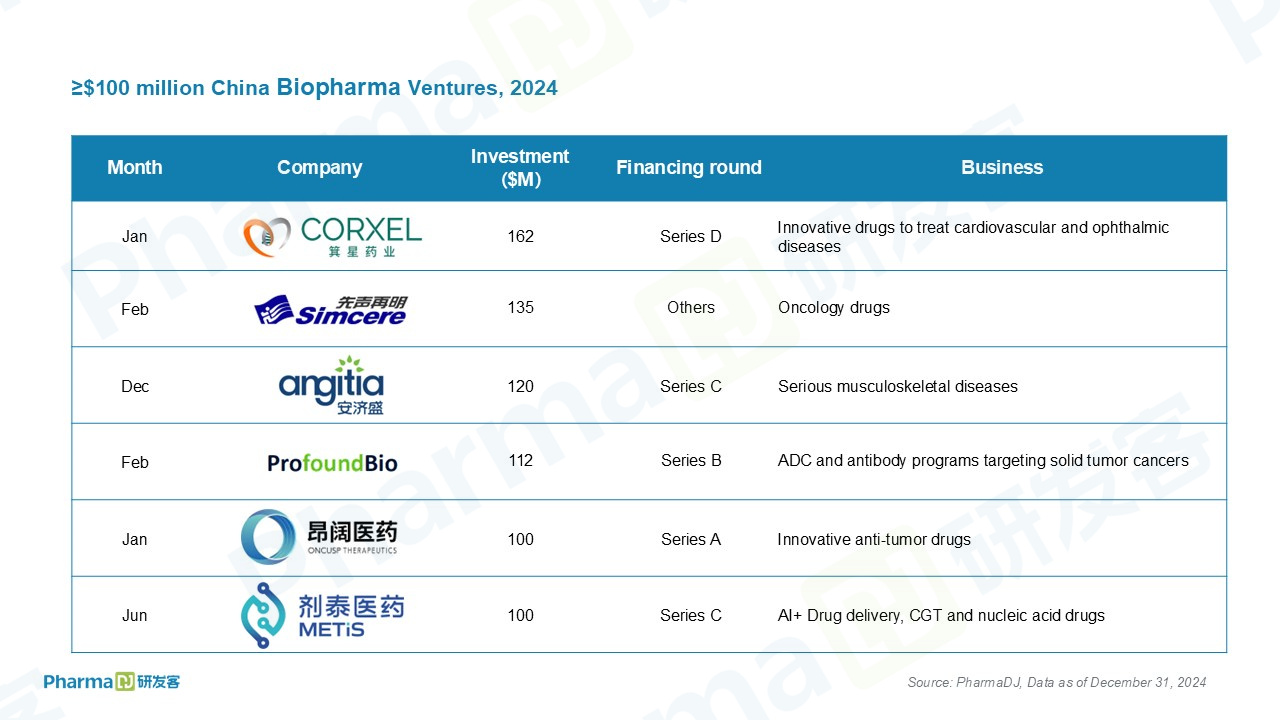

Despite the broader market downturn, six deals surpassed the “mega-round” threshold. Notably, five of these were completed in the first half of the year, while only one—Angitia Biopharmaceuticals—secured funds in December.

Nine Chinese drug developers completed public offerings in 2024. However, due to tightened Chinese listing regulations, no biopharmaceutical companies went public on the A-share market throughout the year.

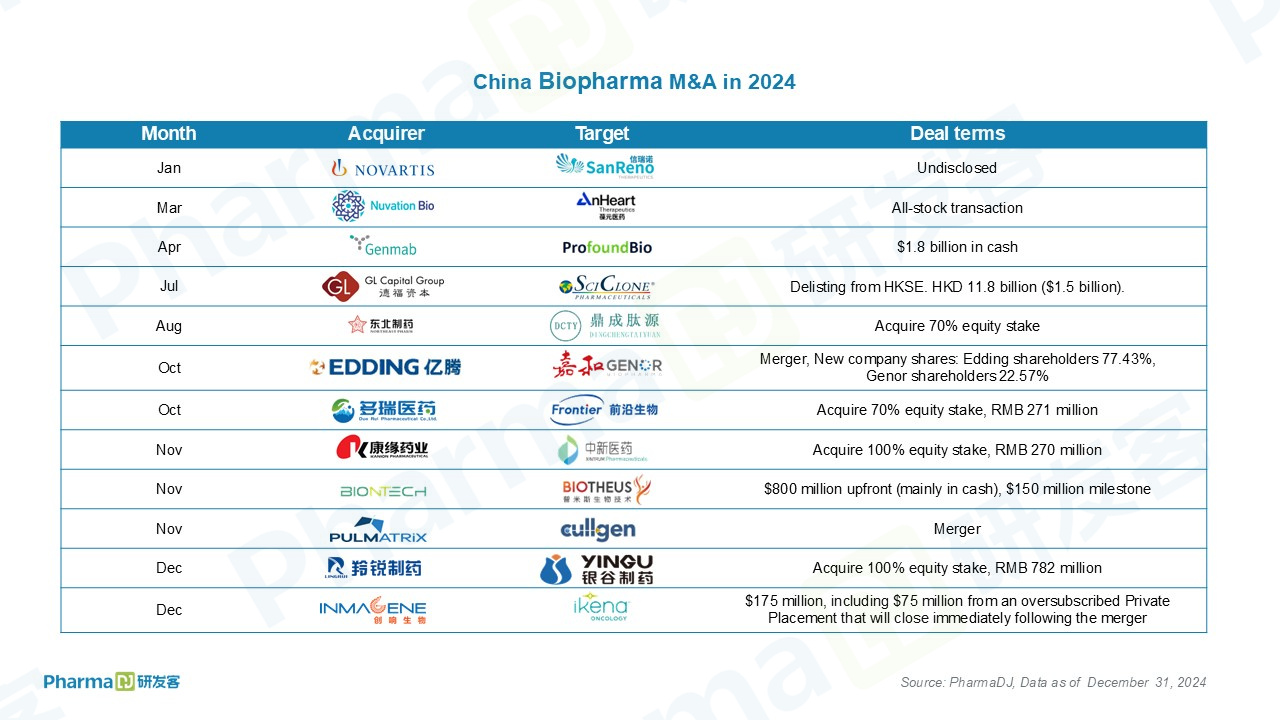

In 2024, there were 12 M&A deals involving Chinese biotech companies. Following the historic acquisition of Gracell by AstraZeneca at the end of 2023—the first instance of a multinational pharmaceutical company acquiring a Chinese biotech—five mergers and acquisitions were completed between multinational pharmaceutical companies and Chinese biotech firms in 2024.

On December 23, Inmagene Biopharmaceuticals, a clinical-stage Chinese biotech company, announced a definitive merger agreement with Ikena Oncology (Nasdaq: IKNA). Upon completion, the combined entity will operate under the name ImageneBio and trade on Nasdaq under the ticker symbol IMA.

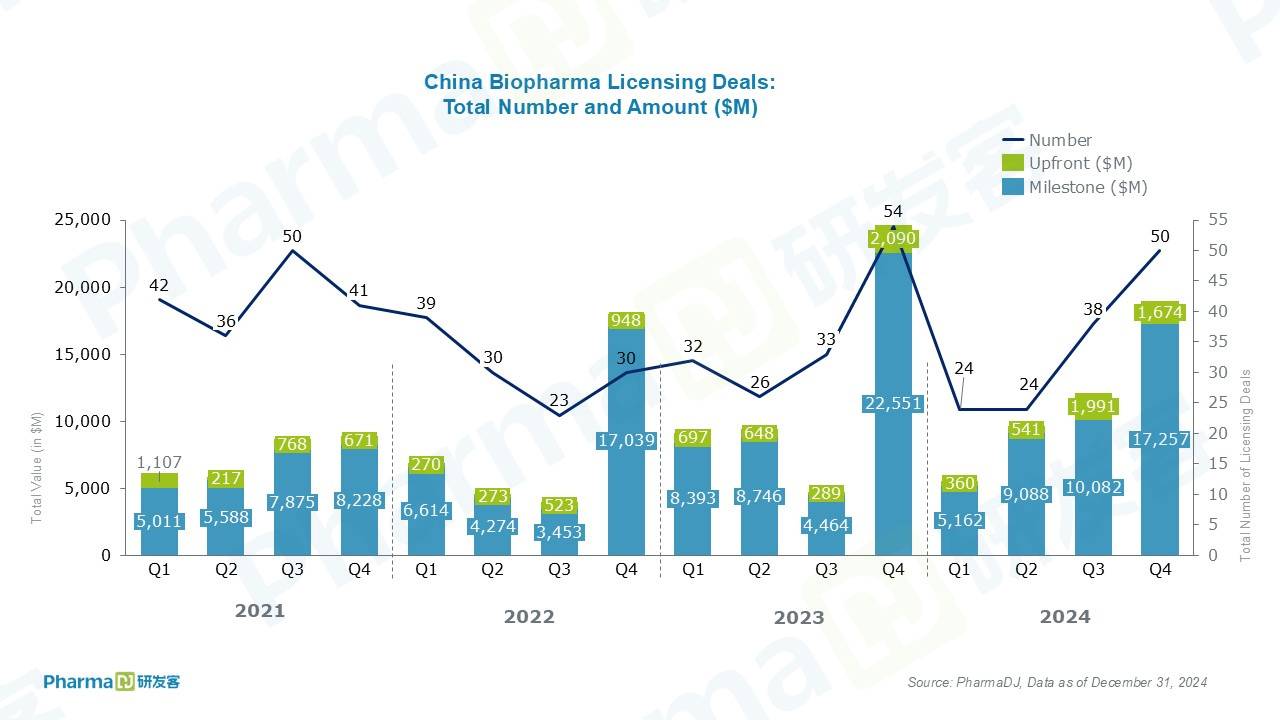

In 2024, there were 136 licensing transactions in China.

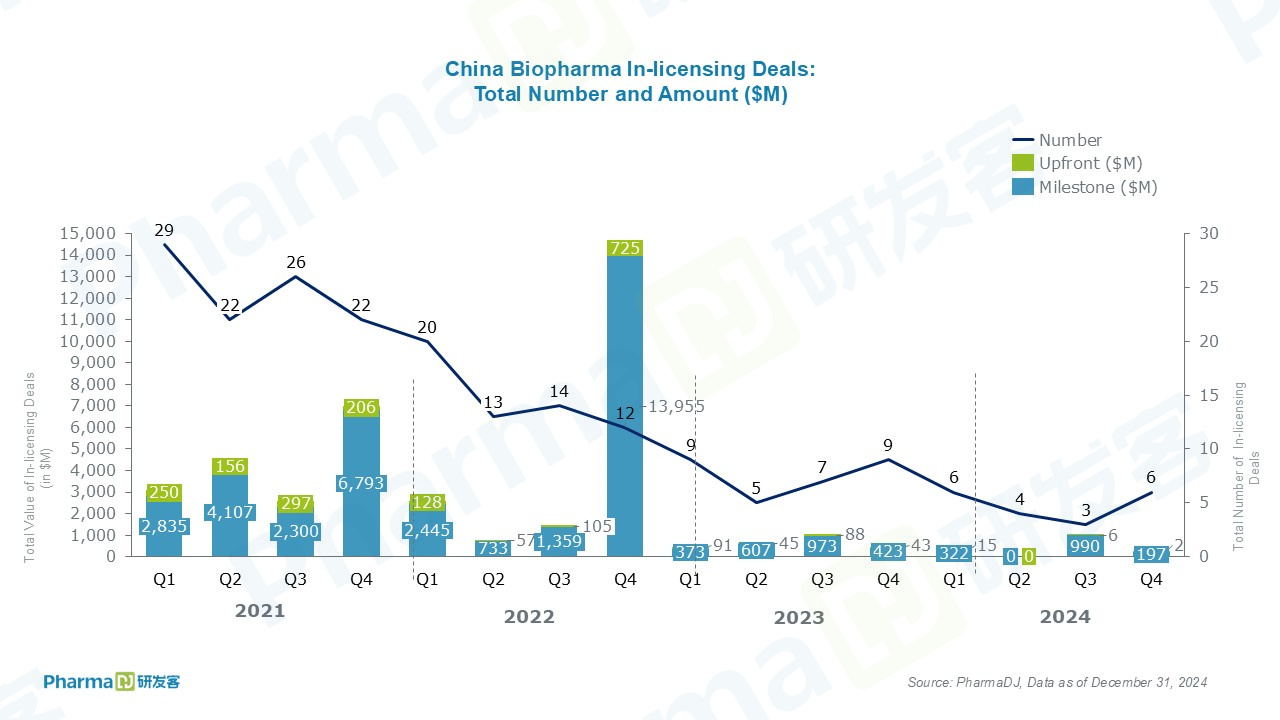

There were 19 in-licensing deals for new assets from overseas, a sharp decline compared to 30 in 2023, 59 in 2022, and 105 in 2021. The total deal value fell to $1.5 billion, down from $2.6 billion in 2023 and $19.5 billion in 2022.

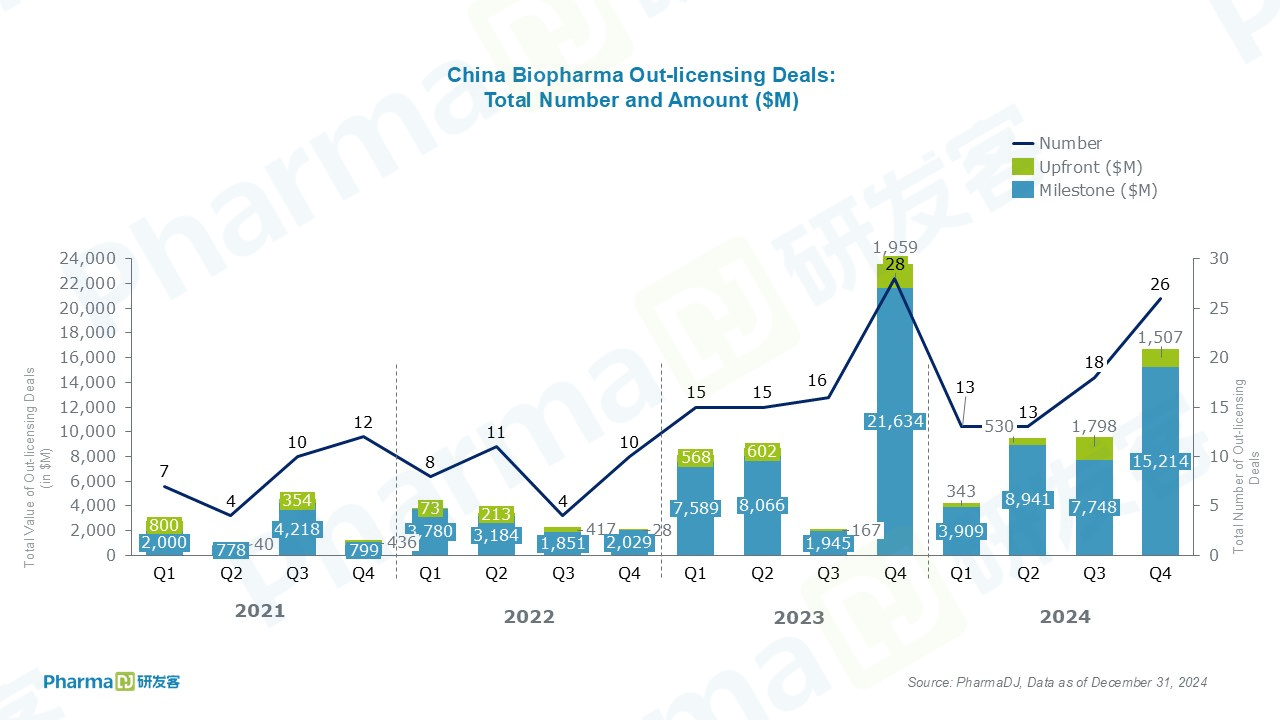

Chinese companies signed 70 out-licensing deals, slightly fewer than 73 in 2023. The total value of these deals reached $40 billion, a slight decline from $42.5 billion in 2023, with $4.2 billion in upfront payments.

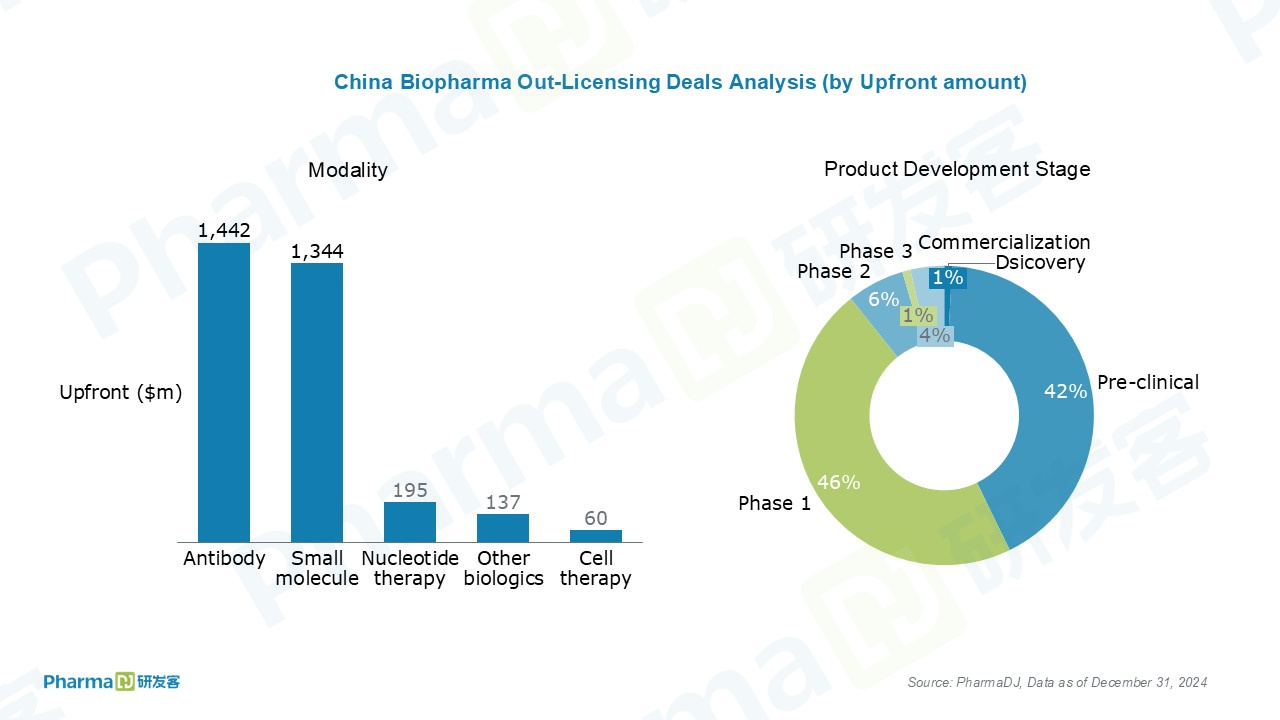

Oncology treatments remained the most significant focus for out-licensing deals. Upfront payments for oncology assets totaled $3.1 billion, accounting for 74% of the total upfront value.

In terms of modalities, antibodies and small molecules received the highest upfront payments. Meanwhile, assets in Phase 1 and preclinical stages attracted the most upfront funding.

In 2024, ten licensing deals with upfront payments exceeding $100 million were announced—all of them out-licensing agreements.