In 2025, China’s biopharmaceutical industry witnessed a dual boom in both capital and transaction markets: total financing volume surged 39% year-on-year, upfront payments for deals jumped 82%, and Newco-model deals hit a historic high of 13. Meanwhile, Hong Kong’s IPO market saw a concurrent uptick in momentum, while mergers and acquisitions (M&A) trended downward.

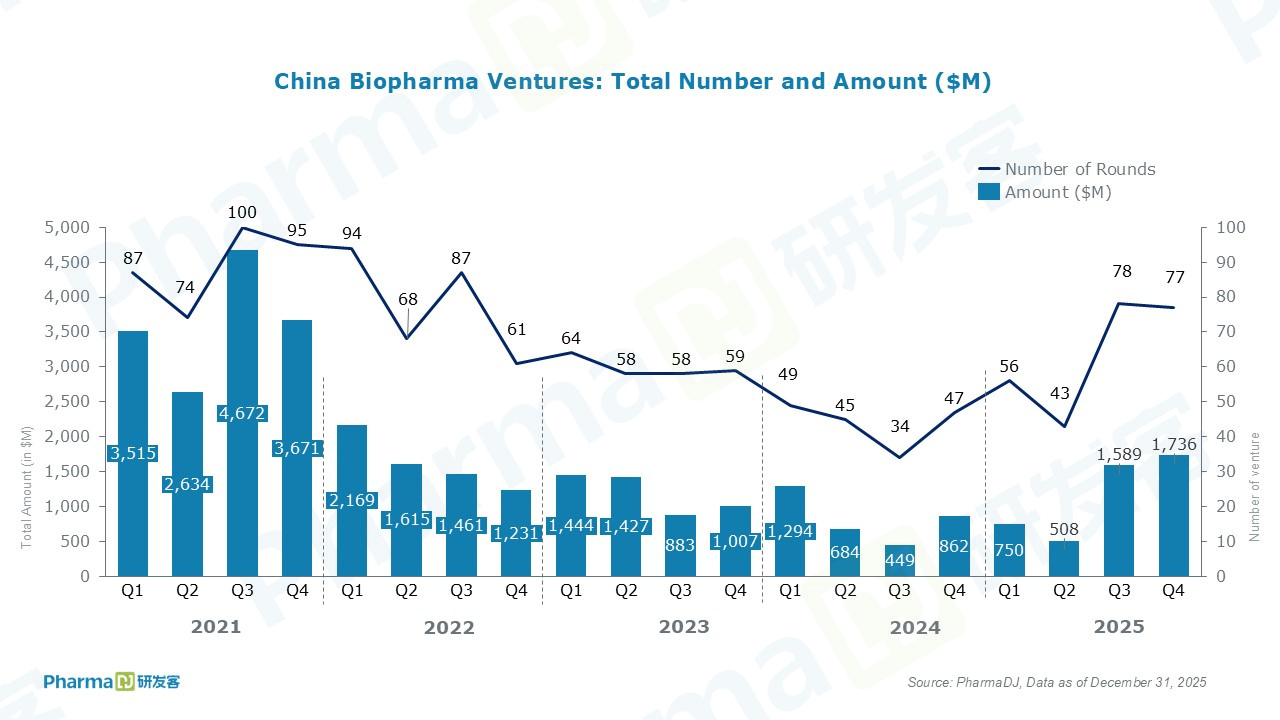

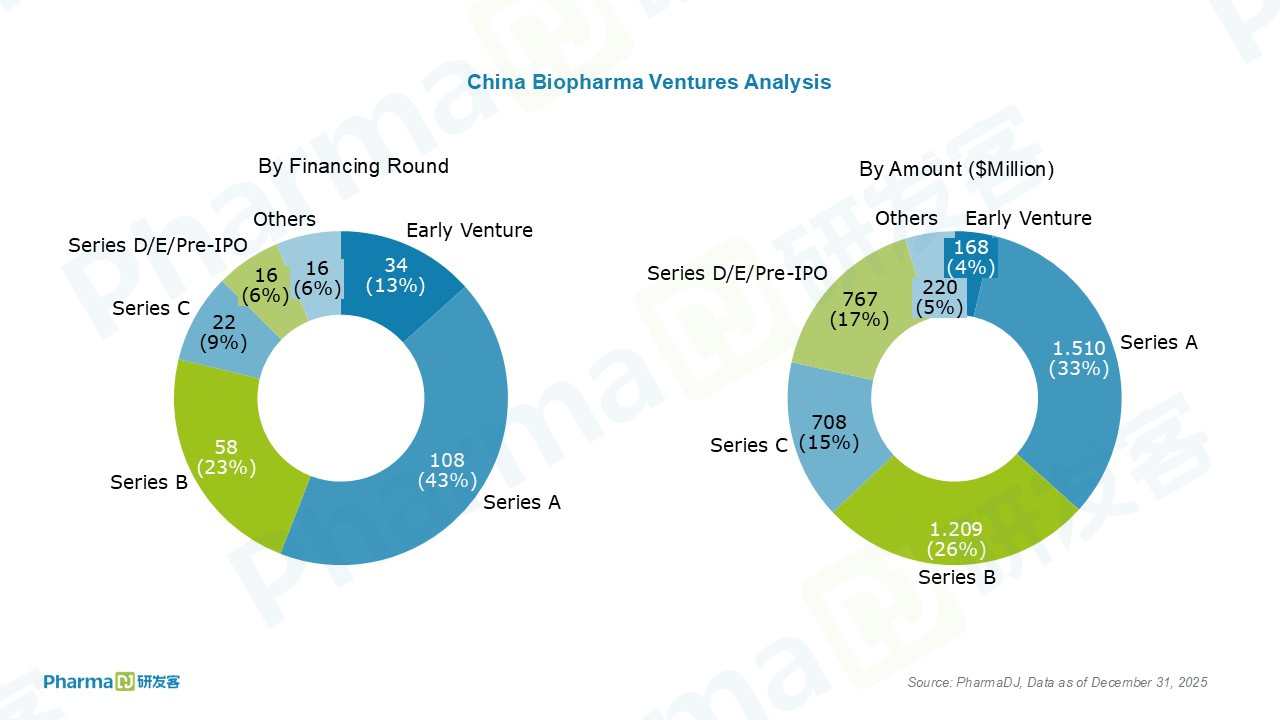

Chinese biopharma financing reached $4.58 billion in 2025, representing a increase of 39% compared with $3.3 billion in 2024. Companies in Series A and Series B rounds captured the majority of the funding.

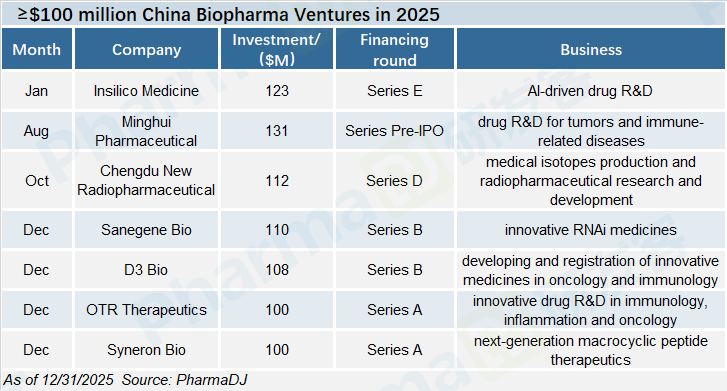

Seven funding deals surpassed the “mega-round” threshold. Notably, four of these were completed in December, namely Sanegene Bio, D3 Bio, OTR Therapeutics and Syneron Bio. This intensive financing drove a mini-boom in December, with the monthly financing volume surging to $950 million, exceeding the combined $788 million raised in October and November.

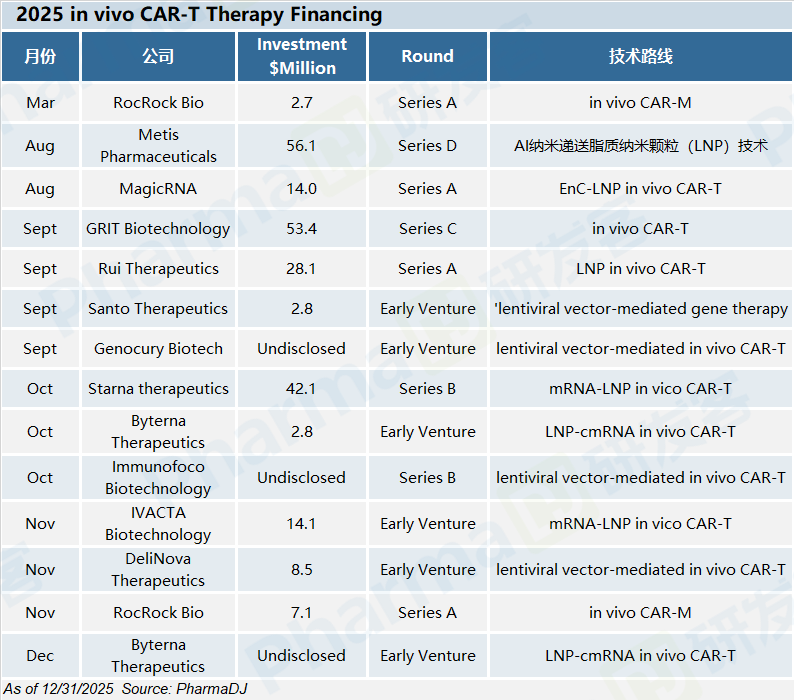

In addition, multinational pharmaceutical companies’ heavy investment in in-vivo CAR-T therapies in 2025 drove a financing boom in the domestic track. Specifically, 12 domestic in-vivo CAR-T enterprises completed 14 financing transactions in 2025, with a total financing volume of $230 million.

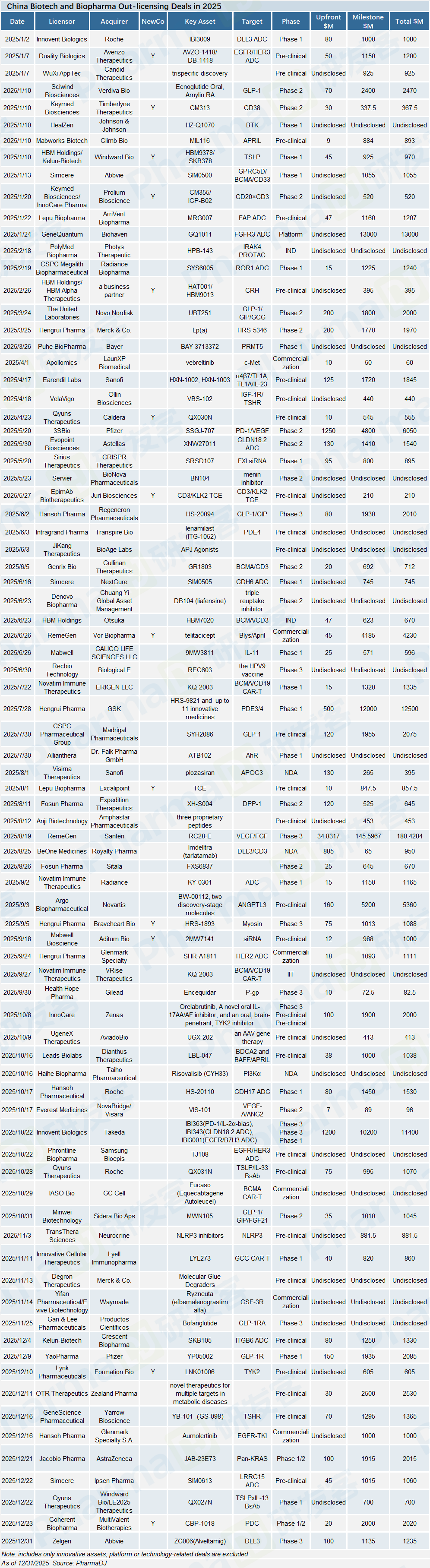

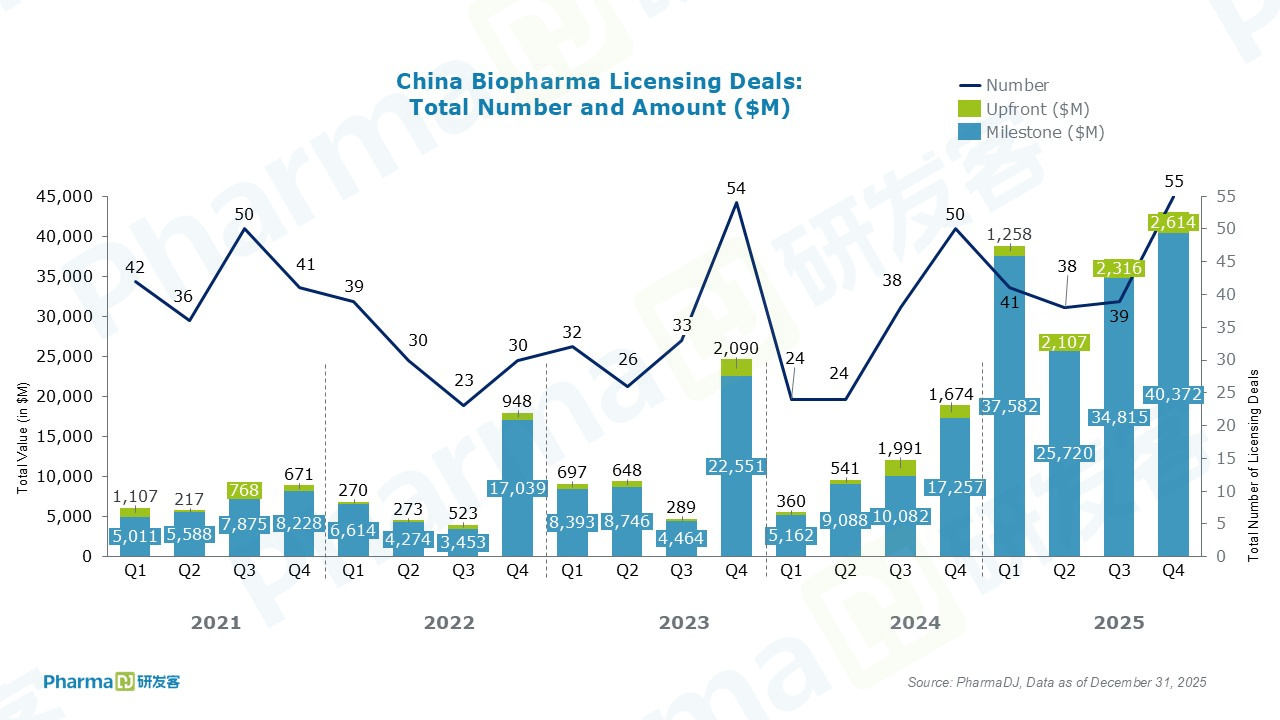

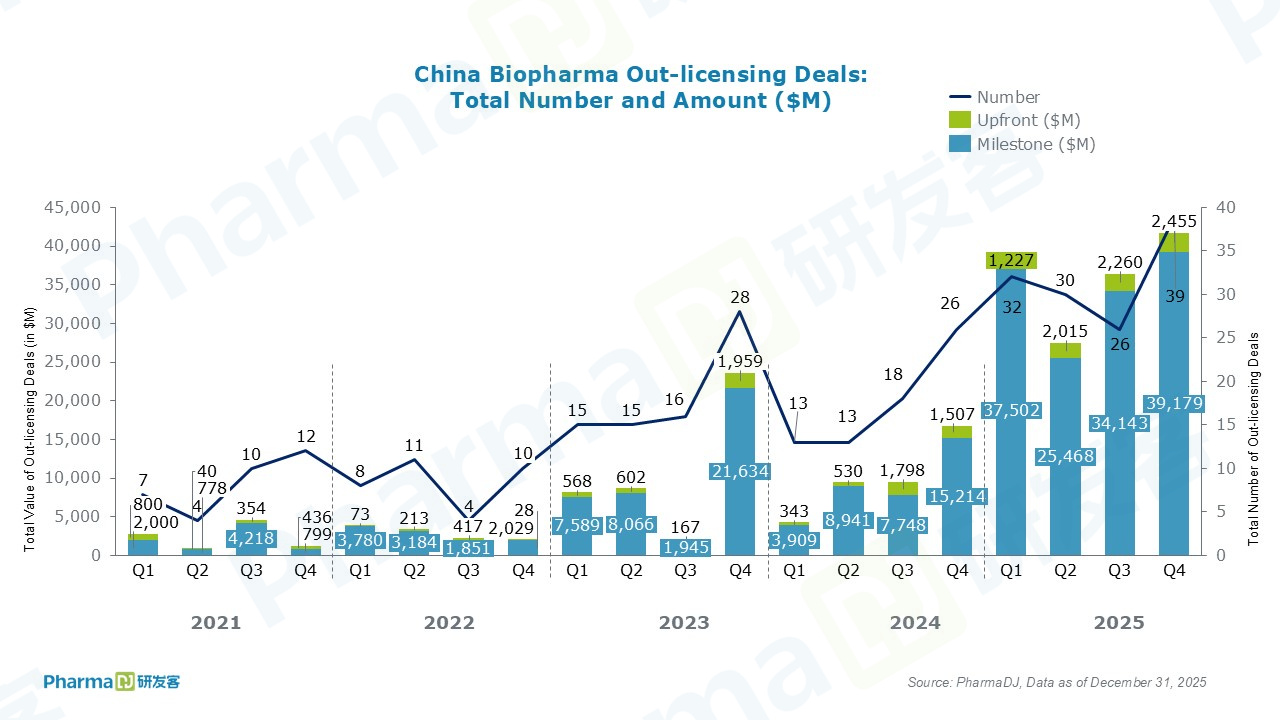

In 2025, China’s biopharmaceutical sector recorded 173 licensing transactions, a significant increase from 136 deals in 2024.

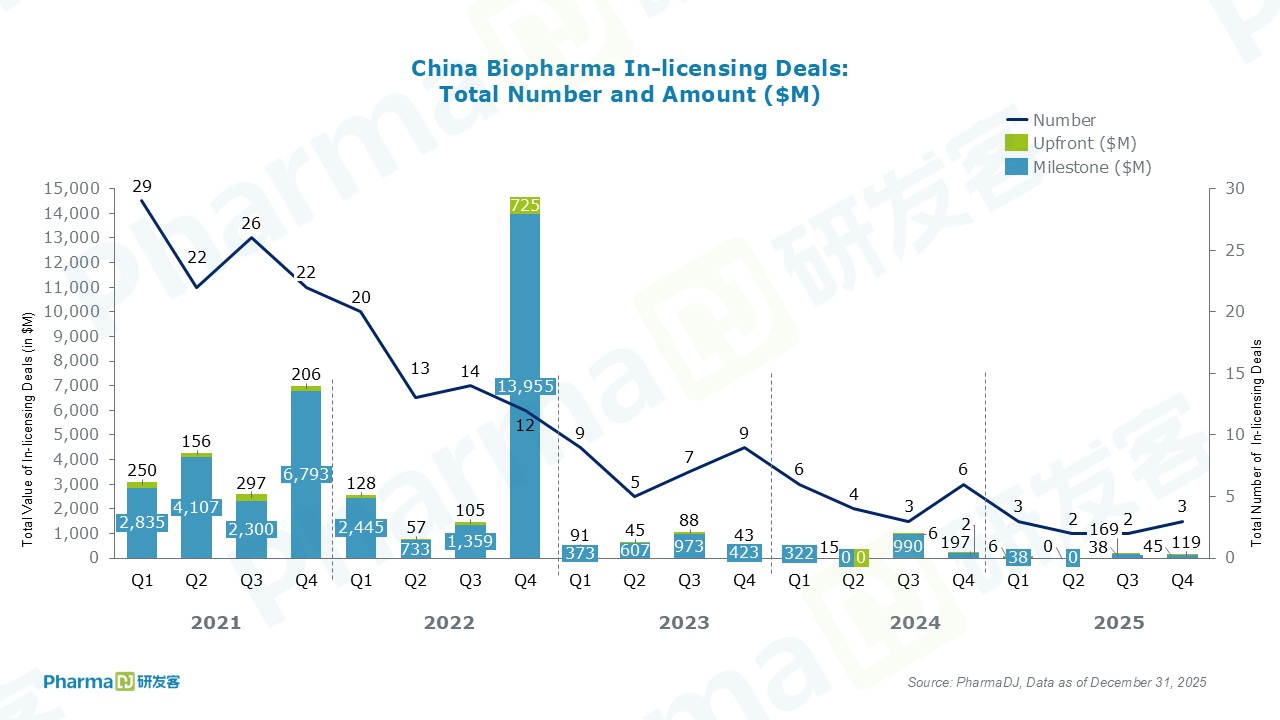

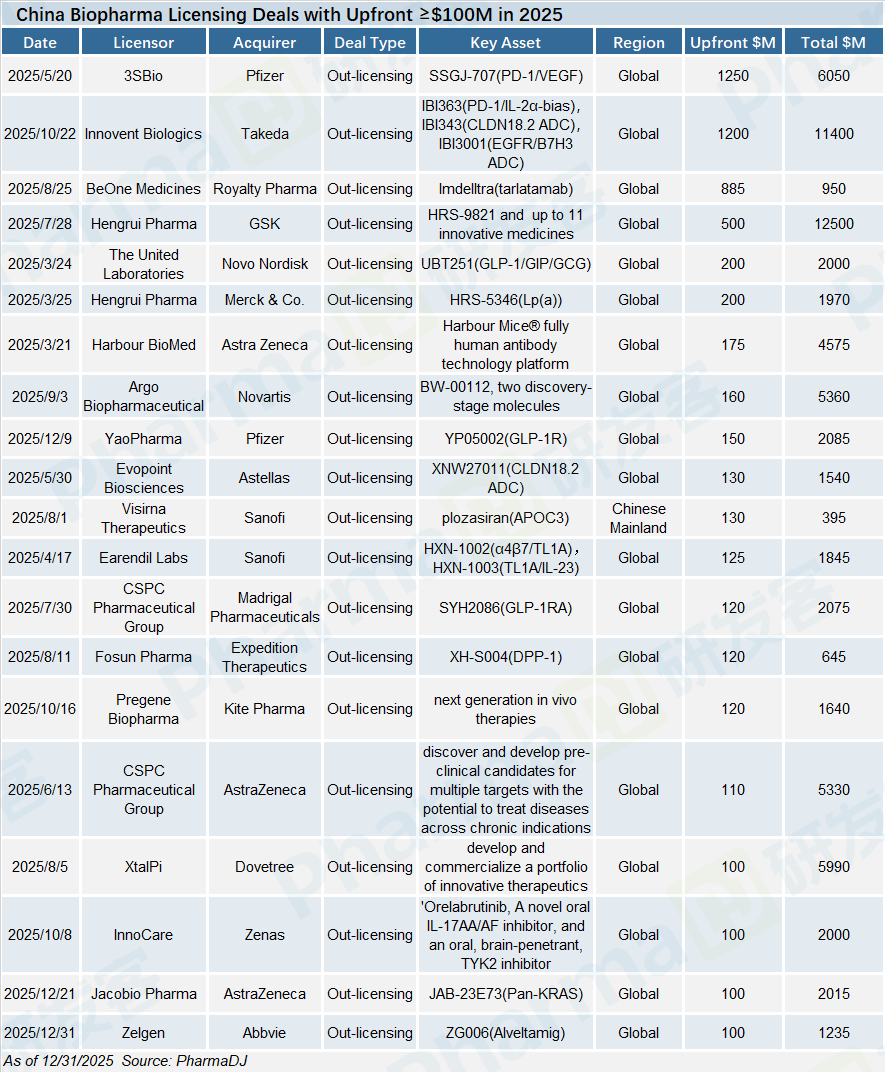

Chinese companies signed 127 out-licensing deals in 2025, with upfront payments and total transaction value reaching $8 billion and $144 billion respectively. Specifically, the number of deals and upfront payments rose by 81% and 90% compared with 2024.

20 licensing deals had upfront payments exceeding $100 million. These deals contributed $6 billion in upfront payments, accounting for 72% of the total annual upfront payments—a figure that surpassed the 2024 full-year upfront payment volume of $4.6 billion.

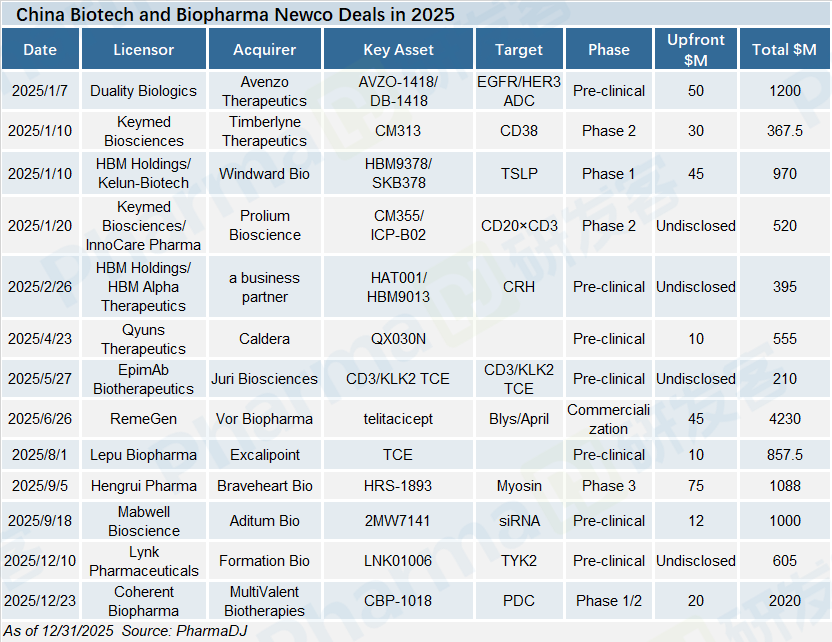

NewCo transactions in 2025 also hit a record high, with 13 deals completed over the year.

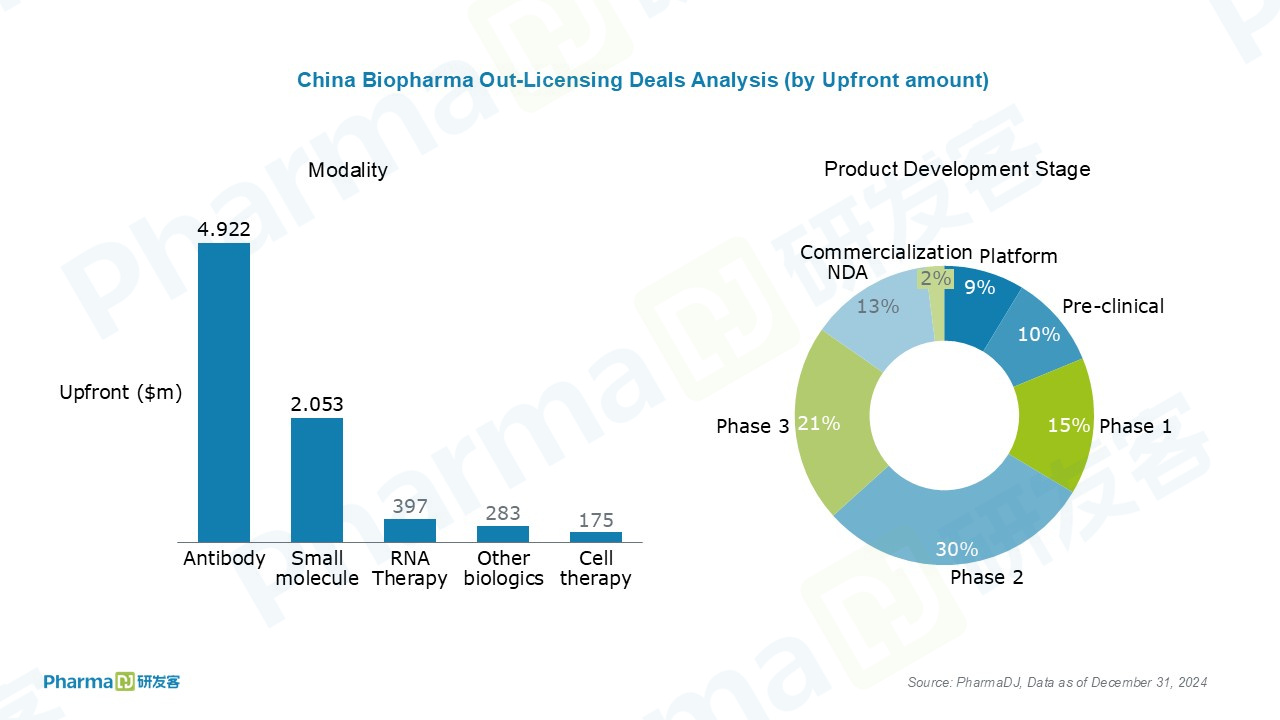

Of the total licensing transactions, antibody drugs (including bispecific antibodies, trispecific antibodies, and ADCs) accounted for the highest share of upfront payments at 62%. Meanwhile, unlike 2024—when preclinical and Phase I assets dominated—Phase II and Phase III stage assets attracted the most upfront funding in 2025.

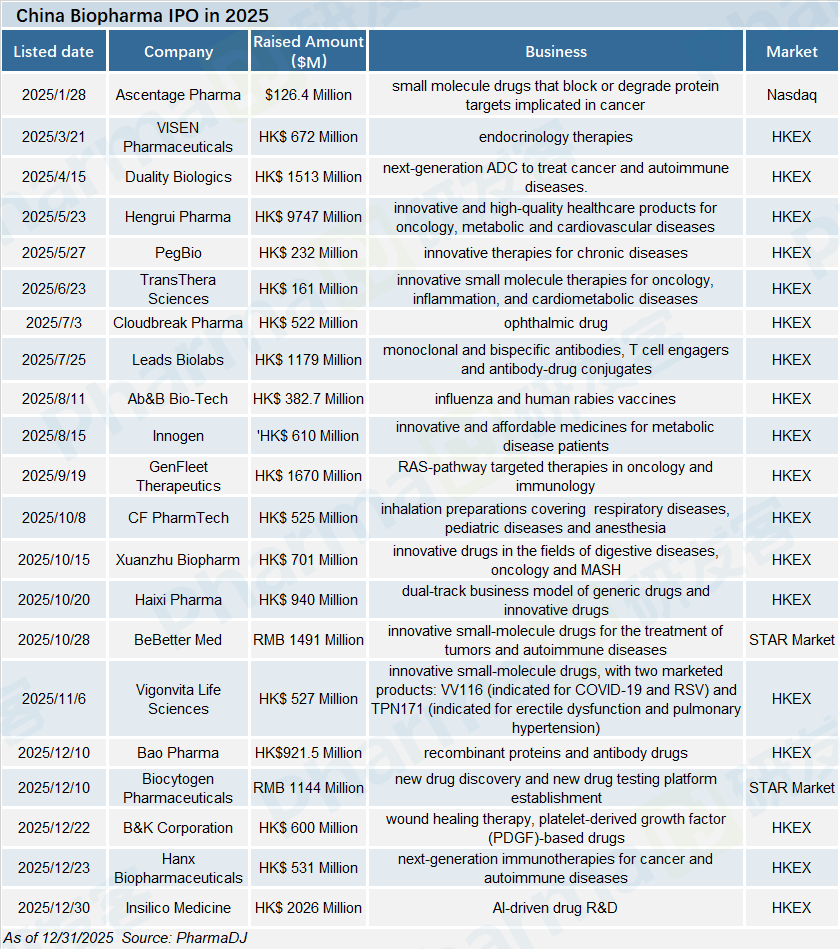

Hong Kong's stock market recovered in 2025, with 18 biotech companies successfully listing on the Hong Kong Stock Exchange (HKEX) over the year, raising a total of HKD 23.5 billion. In addition, Ascentage Pharma listed on the U.S. stock market at the beginning of the year, while Betta Pharma and Biocytogen successfully listed on the Science and Technology Innovation Board (STAR Market) in Shanghai. The total number of listed companies reached 21, far exceeding the 9 in 2024.

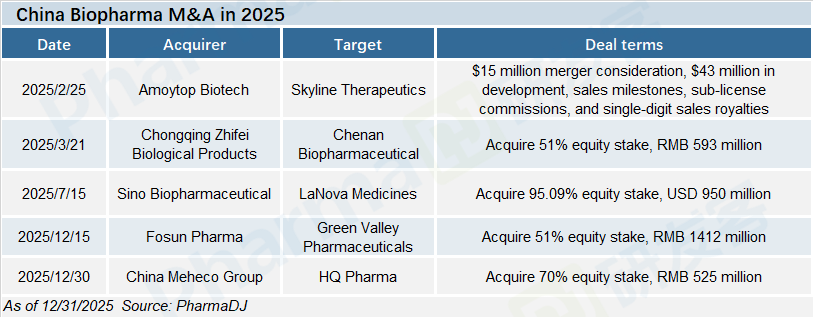

In contrast, the biotech M&A market trended downward in 2025 compared with 2024, with only 5 transactions recorded—down from 12 in the same period a year earlier.